The year 2022 is primarily influenced by the Russian-Ukrainian war. The resulting geopolitical changes caused a state of emergency on the energy markets this year. However, the framework conditions for the energy industry will no longer be the same in the future either: Energy security, diversification as well as efficiency and savings measures are moving to the fore. In the short term, energy prices in the EU have risen to record highs. The consumption of natural gas in Germany has already been reduced year-on-year. In the coming months, too, it will be important to look at the gas import volumes and storage levels.

Geopolitical caesura brings exceptional situation

Since Russia's attack on Ukraine at the end of February 2022, there has been a turning point in Europe. In addition to the tragedies on the ground, the ongoing war is causing geopolitical and economic upheaval around the world. Rising food prices and expensive energy resources are direct effects that hit poorer regions in particular. The sabotage and partial destruction of the Nord Stream 1 and 2 gas pipelines in September 2022 also brought the security and protection of physical energy infrastructure to the fore.

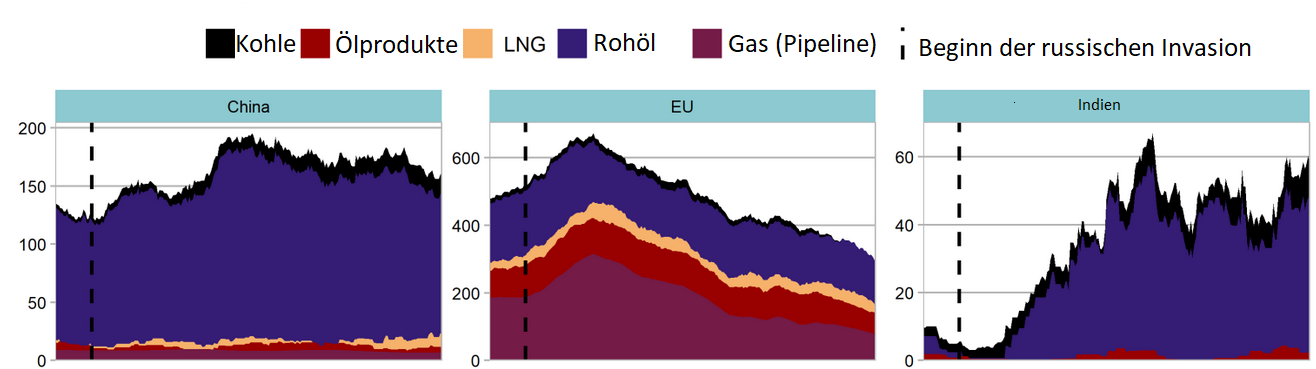

The European countries, which got about 50 percent of their gas imports from Gazprom from Russia before the war, are now changing their minds. Partly because of the decision of the importing countries, partly because of the Russian gas company's supply freeze. Gazprom's delivery volumes to Europe fell by 45 percent in the first eleven months of 2022 compared to the same period last year (source: Montel ). The same applies to imports of hard coal and oil from Russia into the EU. In the medium and long term, Russia will lose its most important buyer of raw materials in the EU. However, other countries absorb some of the amounts, as Figure 1 shows (source: CREA ).

Figure 1: Exports of fossil fuels from Russia in EUR million/day on a 30-day average (source: CREA, 2022) [1]

Extreme prices for electricity and gas

Electricity and gas prices in Europe have been rising since the end of 2021. This was due, among other things, to the relatively low deliveries from Gazprom and the low levels in the storage facilities managed by Gazprom. We report on this in more detail in our article on the price rally on the energy markets . Gas prices in Europe went through the roof when Russia invaded Ukraine. Throughout the summer, Russia gradually halted gas supplies via the Nord Stream 1 gas pipeline. The result: prices rose more than tenfold from pre-war levels. In some blog posts we have analyzed the development of gas and electricity prices in detail (topics: storage targets , spot market prices for electricity andgas market development ).

Figure 2 shows the price development of the most important energy raw materials and emission certificates in European emissions trading from October 2021 to the beginning of December 2022. The extreme price swings up to August 2022 are clearly visible. The decline and stabilization of gas and electricity prices at a high level in autumn 2022 can also be seen.

Figure 2: Percentage development of commodity prices from October 2021 to December 2022 – electricity front year 2023 Germany (candle sticks), gas front year 2023 TTF (yellow line), coal front year 2023 (red line), crude oil Brent Q2 2023 (green line) and EUA Delivery Dec 2023 (orange line) (Source: Montel, 2022) [2]

The drivers for the falling and stable prices towards the end of the year were, on the one hand, the high storage levels for natural gas in Germany and Europe. On the other hand, the gas savings, especially on the part of industry, and the high temperatures played a central role.

Other energy policy developments

In addition to directly dealing with the effects of the Ukraine war, other important decisions for the energy industry were made in 2022. The details are beyond the scope of this article, but the list below should give an overview:

- Abolition of the EEG surcharge as part of the electricity price for end consumers

- Change in the funding conditions for electric vehicles and energy-efficient buildings

- Ambitious targets for the expansion of renewable energies in Germany (80 percent by 2030) in the EEG 2023 and at EU level through REPowerEU

- Energy Security and Energy Saving Act with ordinances to avert a gas shortage

- Start of construction of LNG import terminals to secure gas supply (more on this in the post about LNG terminals )

- Return of (coal) reserve power plants to the electricity market (supply reserve)

- Extension of power generation from nuclear power plants in Germany until mid-April 2023

- Partial nationalization of or entry of the state into gas storage operators (SEFE) and gas importers (Uniper)

- Extensive relief packages for end consumers (electricity and gas price brake)

- Skimming off "excess profits" from electricity producers to finance the price brakes

Decrease in gas consumption, increase in coal and renewables

In the first nine months, primary energy consumption in Germany fell by 2.2 percent, adjusted for weather conditions. A large part of this is due to high energy prices. In particular, the efforts to reduce gas consumption have already been reflected in the statistics, as the working group on energy balances shows (source: AGEB ). Natural gas consumption decreased by 12 percent compared to the first three quarters of 2021. The use of nuclear energy fell by almost 50 percent due to the shutdown of three power plants at the end of 2021. The share of nuclear energy in primary energy consumption was just over 3 percent in the period under review.

In contrast, however, the consumption of coal, particularly in power generation, increased by around 10 percent. The reason for this is the very high gas prices, which make the use of coal-fired power plants more lucrative, and Germany's higher electricity exports to neighboring countries such as France. The use of renewable energies increased by more than 4 percent. From January to the end of September 2022, it covered 17.3 percent of Germany's primary energy needs. Figure 3 shows the percentage changes in primary energy consumption in the first three quarters compared to the same period last year.

Figure 3: Change in primary energy consumption of various energy sources in Q1–Q3 2022 compared to the previous year (source: Energy Brainpool, 2022)

In the period under review, the energy-related CO 2 emissions increased by 2 percent compared to the previous year due to the higher generation of electricity from coal. The greenhouse gas emissions in Germany are therefore not on the target path in 2022 either. Further efforts are necessary to achieve the sectoral targets laid down in the Climate Protection Act.

What will be important in 2023?

The gas crisis was far from over at the end of the year. The temperatures from January to April 2023 in particular determine whether short-term shortages will occur despite the very high fill levels at the beginning of December 2022 and the savings in households and industry. With medium winter temperatures, the gas storage should be able to comply with the legal value of 40 percent by February 1, 2023. This would also simplify refilling next year under the more difficult conditions (significantly fewer Russian gas imports). In summary, this means that the gas storage levels and the LNG import quantities delivered to Germany will continue to follow us in 2023.

The medium and long-term changes that are being discussed at EU level, but also in Germany, with regard to the design of the electricity market are still groundbreaking. A working group made up of important stakeholders is to present proposals for Germany in the coming year. The introduction of a capacity market or tradable contributions to security of supply in Germany is on the agenda.

In addition to the acute problems in the energy industry due to the war in Ukraine, the focus on reducing emissions must not be let up. Important decisions on this are still pending in the EU trilogues on the “Fit for 55” package in 2023. It will also be decisive how strongly the expansion of renewable energies is actually progressing and whether approval procedures can be accelerated. The goal of 80 percent renewable electricity can only come within reach if the course is set for this next year.

References of the illustrations:

[1] CREA, 2022

[2] Montel, 2022